May 11, 2023

If there were a risk-free investment allocation in which the Alaska Permanent Fund could achieve its long-term return objective of 5% plus inflation, the Fund’s investment management would be relatively straightforward. Realistically, it is not possible to achieve this targeted return safely through any single investment or asset class.

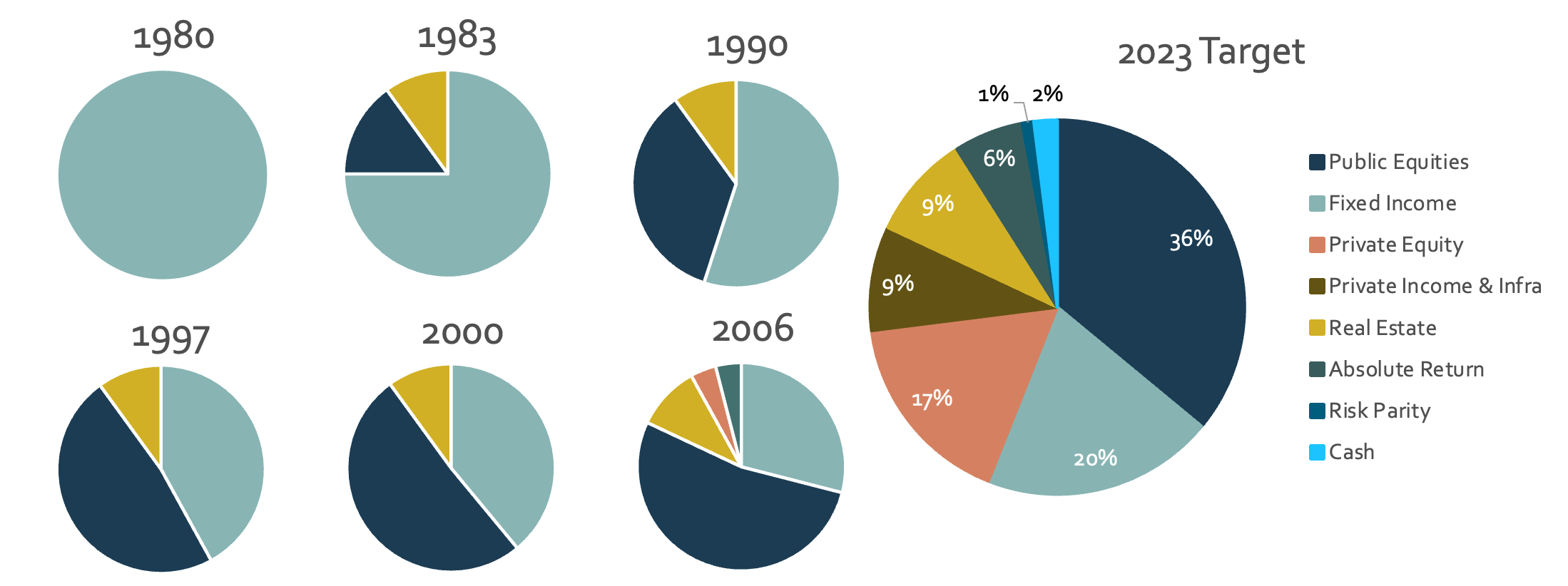

Before the 1980s, governments generally had more regulations related to investment options for their public funds. In the 1950s, with higher interest rates and bond yields available, more than 95 percent of public fund investments were in fixed income and cash. In the late 1980s and 1990s, as it became more difficult to achieve targeted returns through only fixed income, governance restrictions relaxed and funds transitioned portfolios from solely fixed income to include stocks. By the 1990s, the average fixed income allocation had decreased to nearly 45 percent, and other more risky assets were included. By the 2020s, the average public fund portfolio held approximately 23 percent of fixed income and cash assets.

Portfolio Progression

Investment strategy for the Alaska Permanent Fund has mostly followed that same path over the years. When first established in 1976, the Fund was invested in only one asset class, US treasuries. When APFC was created to manage the assets in 1980, the Corporation worked with the State Legislature to identify in statute the allowable investments for the portfolio.

In 2005, as the Fund grew, the Legislature put more trust in the Corporation to make sound financial decisions by following the prudent investor rule. With the increased latitude provided to the Board, they began to develop a more diversified and sophisticated portfolio, including traditional and alternative assets, intended to generate higher returns associated with higher risk.

Informed by advice from staff and investment consultants, the Board of Trustees maintain a long-term, 10-year horizon when making allocation adjustments every year as part of their annual Investment Policy review. To best protect the Principal and diversify the portfolio to maximize risk-adjusted returns over time, APFC’s Board of Trustees considers all possible portfolio construction options.

APFC portfolio construction over time

“Over the history of the Corporation, the Board has built an increasingly diverse Fund portfolio to maximize returns while remaining conservative enough to protect the Principal, our primary duty. Maintaining a long-term perspective helps ensure that the modest portfolio adjustments, thoughtful guidance, and direction we develop will consistently support the Fund’s ability to generate a valuable return for Alaskans,” observes Board of Trustees Chair Ethan Schutt.

Portfolio Optimization and Implementation

Since target asset allocation changes aren’t made in reaction to daily market news, as investment managers of the Permanent Fund, APFC remains focused more on improving execution rather than predicting what markets might look like over the near term. Execution describes APFC’s pursuit of individual strategies with discipline and skill, such as backing alternatives’ managers with specific characteristics based on rigorous analysis, or maintaining strong underwriting discipline on new real estate acquisitions.

The practical approach to implementing a strategic asset allocation is the responsibility of APFC’s Chief Investment Officer, Marcus Frampton, who starts with a theoretical exercise called portfolio optimization.

“Optimization is a complex statistical process that models a variety of portfolio options with different characteristics against predicted future returns,” explains Marcus, who uses the tool to produce a type of chart called an efficient frontier. The efficient frontier projects the maximum expected returns for various portfolios at any given risk threshold. Each asset class has three variables used for optimization; expected return; standard deviation – a measure of volatility; and correlation to each asset class included in the optimization.

The theory for the efficient frontier is attributed to Harry Markowitz, an economist awarded the Nobel Prize for his revolutionary work developing the Modern Portfolio Theory. Markowitz’s strategy recognized that the performance of individual assets within a portfolio was not necessarily as important as the performance or composition of the total portfolio. Markowitz said, “A good portfolio is more than a long list of good stocks and bonds. It is a balanced whole, providing the investor with protections and opportunities with respect to a wide range of contingencies.”

The theory for the efficient frontier is attributed to Harry Markowitz, an economist awarded the Nobel Prize for his revolutionary work developing the Modern Portfolio Theory. Markowitz’s strategy recognized that the performance of individual assets within a portfolio was not necessarily as important as the performance or composition of the total portfolio. Markowitz said, “A good portfolio is more than a long list of good stocks and bonds. It is a balanced whole, providing the investor with protections and opportunities with respect to a wide range of contingencies.”

Defining the parameters used for optimization takes considerable experience, skill, and access to good data. Based on the investor’s views on market conditions and asset class characteristics, the optimizer uses historical performance, cyclical business activity, and future projections to generate an outlook for a portfolio’s characteristics.

Another calculation APFC uses to model projected returns is the Shiller PE Ratio. It considers the valuation of a stock or a market versus its earnings, adjusted for the business cycle over a 10-year period. The long-term perspective of this measurement helps smooth out short-term volatility fluctuations giving investors a better understanding of the current value of an individual stock or the overall market.

Conservative positioning

The Shiller PE Ratio shows that the stock market is currently considered expensive by historical standards. The Shiller PE levels that have prevailed in the past few years have only been seen twice– in 2000 and 1929. Significant market disruptions and large economic recessions followed both of those years.

“As far as I can tell, virtually everyone in the industry has progressively built riskier and riskier portfolios over the last 20 years,” says Marcus Frampton. “I can’t think of a single major plan that reduced risk during my professional career.”

Having recently been in a bull market that lasted more than ten years, many economists and governments predict a recession within the next year. Frampton believes that certain asset classes will be impacted more than others and that public funds, especially those that experience higher than tolerable losses in the next cycle, will move towards more conservative portfolios.

Despite the industry-wide trend to shift towards more risky assets, over the past five years, APFC has attempted to err on the side of conservatism. For example, the Corporation has materially reduced annual commitment volume to riskier areas such as private equity and infrastructure investments.

“Swimming against the current for the last five years, I’m surprised that we’ve had as strong of relative performance as we have,” says Frampton, “We’ve generally held extra cash cushion in our portfolio and maintained discipline in the annual deployment to riskier areas. I believe we can continue to deliver performance in excess of our benchmark and top quartile among peer plans through strong execution.”

Through a well-positioned portfolio, invested across eight diverse asset classes, Frampton and his team continue to identify investments with expected returns that meet the Fund’s long-term objectives. With the diversified portfolio, the Fund has also felt less impact from increasing interest rates over the past year. Furthermore, the Fund’s allocations to gold and other real assets are expected to help protect it from the long-term impacts of inflation.

“With the strategy that we’ve developed,” says Marcus, “I believe that the Fund can stand out as a top-performing institutional investor even in quite difficult market scenarios.”